December 11, 2019

GENCOR RELEASES FOURTH QUARTER AND FISCAL YEAR 2019 RESULTS

FOR IMMEDIATE RELEASE:

December 11, 2019 (PRIME NEWSWIRE) – Gencor Industries, Inc., (NASDAQ: GENC) announced today net revenue for the quarter ended September 30, 2019 decreased 29.5% to $14.5 million compared to $20.5 million for the quarter ended September 30, 2018. Gross profit as a percentage of net revenue decreased to 19.6% for the quarter ended September 30, 2019 from 31.8% for the quarter ended September 30, 2018. Gross profit in the fourth quarter of fiscal 2019 was negatively impacted due to the lower net revenues and reduced overhead absorption.

Operating loss for the quarter ended September 30, 2019 was ($0.5) million compared to operating income of $3.5 million for the quarter ended September 30, 2018. The Company had non-operating income of $0.6 million for the quarter ended September 30, 2019 compared to $1.2 million for the quarter ended September 30, 2018. The Company’s tax expense was $0.1 million for the quarter ended September 30, 2019 compared to $0.9 million for the quarter ended September 30, 2018. Net income for the quarter ended September 30, 2019 was breakeven compared to $3.9 million ($0.27 per basic and diluted share) for the quarter ended September 30, 2018.

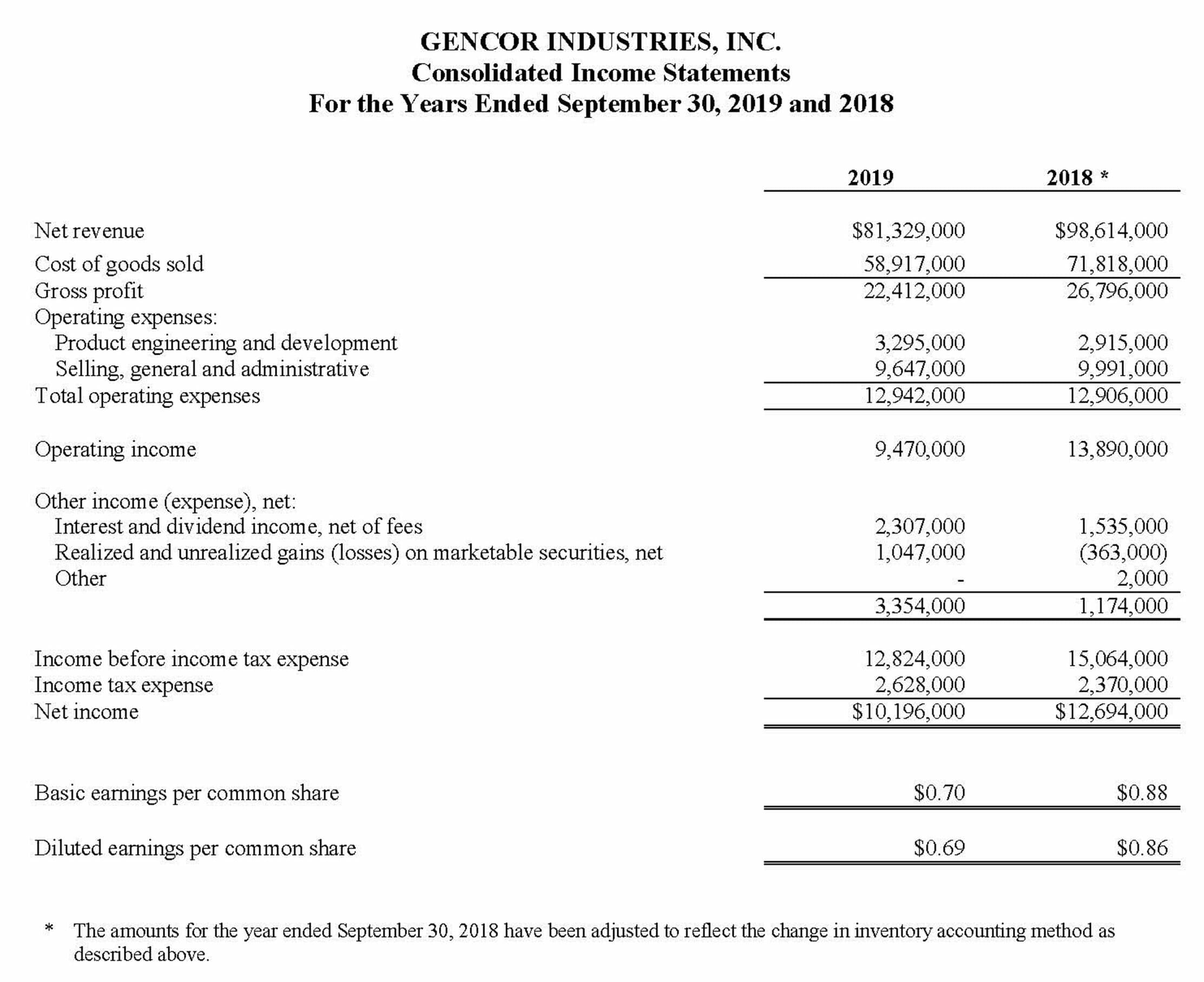

Net revenue for the year ended September 30, 2019 decreased 17.5% to $81.3 million compared to $98.6 million for the year ended September 30, 2018. Gross profit as a percentage of net revenue increased to 27.6% for the year ended September 30, 2019 from 27.2% for the year ended September 30, 2018. The Company had operating income for the year ended September 30, 2019 of $9.5 million compared to $13.9 million for the year ended September 30, 2018. The Company had non-operating income of $3.4 million for the year ended September 30, 2019 compared to $1.2 million for the year ended September 30, 2018.

On December 22, 2017, the U.S. Tax Cuts and Jobs Act (the “Tax Reform Act”) was signed into law by President Donald Trump. The Tax Reform Act significantly lowered the U.S. corporate federal income tax rate from 35% to 21% effective January 1, 2018, while also implementing a territorial tax system and imposing repatriation tax on deemed repatriated earnings of foreign subsidiaries. Accounting principles generally accepted in the United States of America (“GAAP”) require that the impact of tax legislation be recognized in the period in which the law was enacted. The effective income tax rate for fiscal 2019 was 20.5% versus 15.7% in fiscal 2018.

The Company’s net income was $10.2 million ($0.70 per basic share and $0.69 per diluted share) for the year ended September 30, 2019, compared to $12.7 million ($0.88 per basic share and $0.86 per diluted share) for the year ended September 30, 2018.

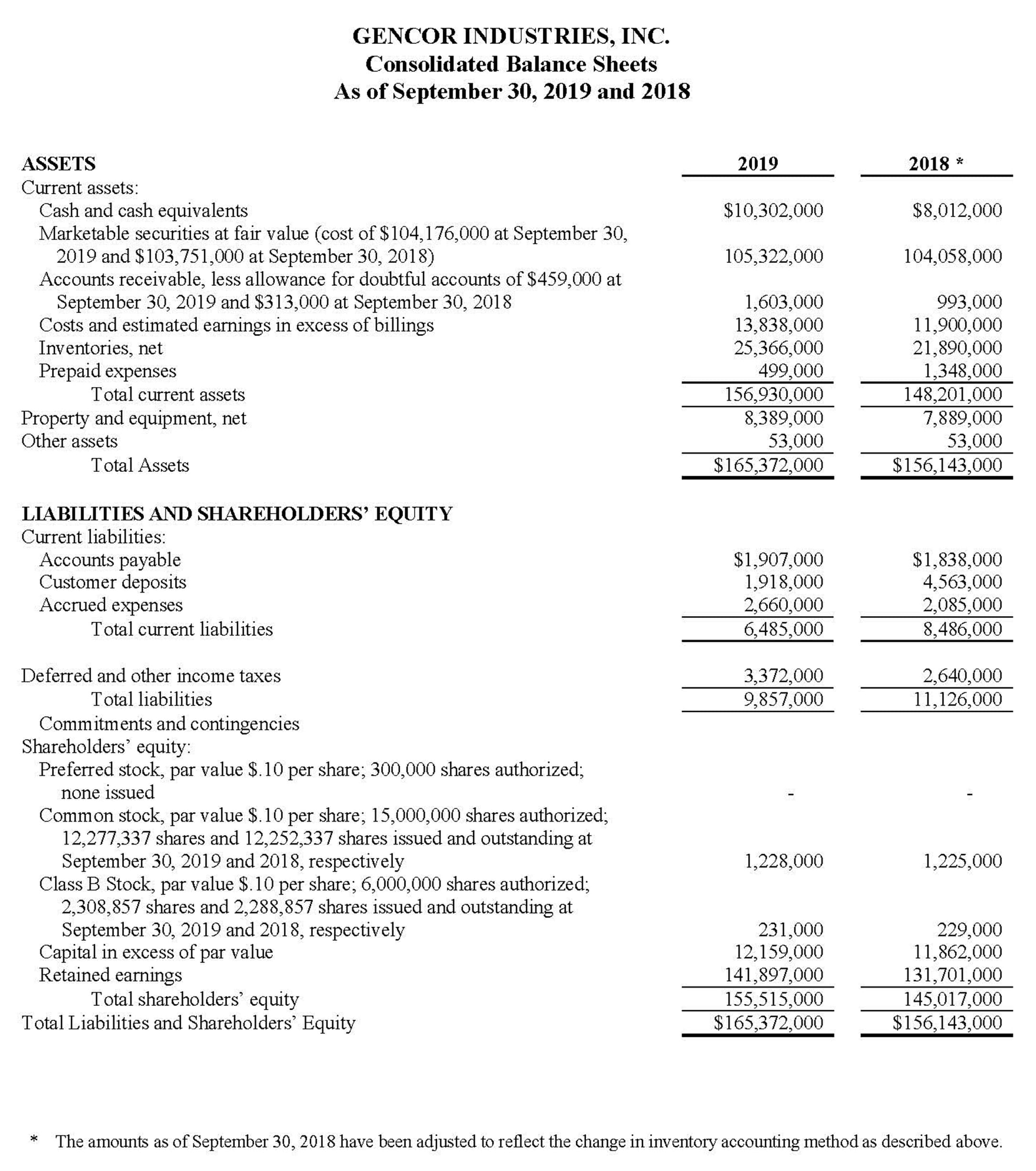

At September 30, 2019, the Company had $115.6 million in cash and marketable securities, an increase of $3.5 million over the September 30, 2018 balance of $112.1 million. Net working capital was $150.4 million at September 30, 2019. The Company has no short- or long-term debt.

The Company’s backlog was $27.3 million at December 1, 2019 compared to $28.0 million at December 1, 2018.

During the fourth quarter of fiscal 2019, the Company changed its method for accounting for cost of inventories from the last-in, first-out (“LIFO”) method to the first-in, first-out (“FIFO”) method. The Company believes the FIFO method will improve financial reporting by better reflecting the current value of inventory on the condensed consolidated balance sheets, by more closely aligning the flow of physical inventory with the accounting for the inventory, and by providing better matching of revenues and expenses. As required by GAAP, the Company has reflected this change in accounting principle on a retrospective basis, resulting in changes to the historical periods presented. The retrospective application of the change resulted in an increase in the Company’s September 30, 2018 retained earnings of $2.8 million (net of $0.8 million in taxes) and an increase to the Company’s net income of $130,000 (net of $45,000 in taxes) for the year ended September 30, 2018. This change did not affect our previously reported cash flows from operating, investing or financing activities nor did it have a material impact on the previously reported quarterly operating results for fiscal 2019.

John E. Elliott, Gencor’s CEO, commented, “Gencor’s fourth quarter results reflect a more typical level of production, as the increase orders we enjoyed in recent years as a result of the FAST Act have tempered. The FAST Act is scheduled to expire in 2020. Currently, there is no approved Federal infrastructure bill to replace the FAST Act although the recently passed resolutions did include continued funding of the FAST Act through 2020.

In the second half of fiscal 2019 we experienced a normal ordering pattern where customers place large equipment and plant orders in the latter part of the year, with the expectation of delivery in the late winter and early spring months. We have been able to respond to changes in the market place by ramping up production when demand increased from 2016 to 2018 and reducing production levels as demand has normalized. We plan to continue cost improvements and to adjust production based on demand, to maximize productivity and profitability.

Fourth quarter revenues of $14.5 million were below fourth quarter fiscal 2018 record revenues of $20.5 million. Gross margin of 20% were also lower, due to the lower net revenues and reduced overhead absorption.

After the fiscal year ended, we are benefitting from an increase in orders for production and delivery in fiscal 2020. As we prudently increased stocking inventory in the summer months, we have converted this inventory to revenue more quickly which has allowed us to accelerate our typical lead time on equipment.

We believe we are well-positioned to capitalize on demand for asphalt plants and related components as we continue to strategically invest in our business. We continue to take action to reduce the impact of U.S. tariff policies, raw material volatility and a continued tight labor market.”

Gencor Industries is a diversified heavy machinery manufacturer for the production of highway construction materials, synthetic fuels and environmental control machinery and equipment used in a variety of applications.

Caution Concerning Forward Looking Statements – This press release and our other communications and statements may contain “forward-looking statement,” including statement about our beliefs, plans, objectives, goals, expectations, estimates, projections and intentions. These statements are subject to significant risks and uncertainties and are subject to change based on various factors, many of which are beyond our control. The words “may,” “could,” “should,” “would,” “believe,” “anticipate,” “estimate,” “expect,” “intend,” “plan,” “target,” “goal,” and similar expressions are intended to identify forward-looking statements. All forward-looking statements, by their nature, are subject to risks and uncertainties. Our actual future results may differ materially from those set forth in our forward looking statements. For information concerning these factors and related matters, see our Annual Report on Form 10-K for the year ended September 30, 2019: (a) “Risk Factors” in Part I, Item 1A and (b) “Management’s Discussion and Analysis of Financial Position and Results of Operations” in Part II, Item 7. However, other factors besides those referenced could adversely affect our results, and you should not consider any such list of factors to be a complete set of all potential risks or uncertainties. Any forward-looking statements made by us herein speak as of the date of the press release. We do not undertake to update any forward-looking statement, except as required by law.

Contact: Eric Mellen, Chief Financial Officer

407-290-6000